Answer:

Note: The question is attached as a picture

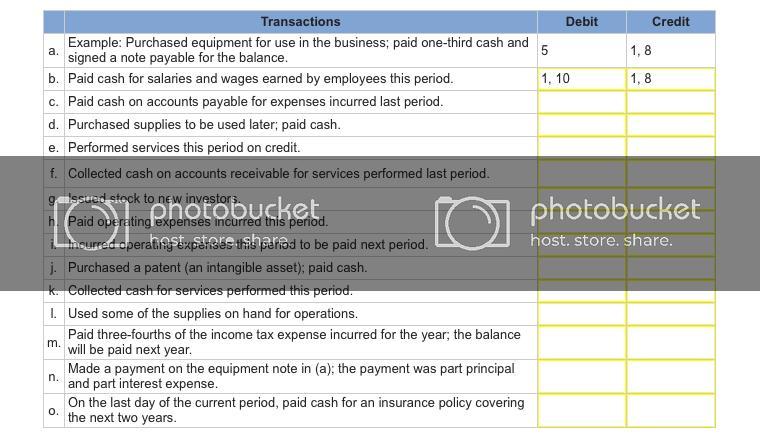

(a) An example is shown below

(b) Dr 15. Operating Expenses (wages, supplies)

Cr 1. Cash

(c) Dr 7. Account Payable

Cr 1. Cash

(d) Dr 3. Supplies

Cr 1. Cash

(e) Dr 2. Accounts Receivable

Cr 14. Service Revenue

(f) Dr 1. Cash

Cr 2. Accounts Receivable

(g) Dr 1. Cash

Cr 11. Common Stock

(h) Dr 15. Operating Expenses (wages, supplies)

Cr 1. Cash

(i) Dr 15. Operating Expenses (wages, supplies)

Cr 9. Wages Payable

(j) Dr 6. Patent

Cr 1. Cash

(k) Dr 1. Cash

Cr. 14. Service Revenue

(l) Dr 15. Operating Expenses (wages, supplies)

Cr 3. Supplies

(m) Dr 16. Income Tax Expense

Cr 1. Cash

Cr. 10. Income Tax Payable

(n) Dr 8. Note Payable

Dr 17. Interest Expense

Cr 1. Cash

(o) Dr 4. Prepaid Expense

Cr 1. Cash

Response:

option c.

Clarification: an ongoing tracking system

Answer:

C. Determine Requirements

Explanation:

Those responsible for managing resources must initially determine the requirements for those resources.

Requirement determination involves assessing how many resources are needed, where they will be utilized, and who will receive them.

Resource needs can vary depending on the circumstances at hand. When we speak of resource requirements, we refer to both the types and amounts of resources essential for the successful fulfillment of a project.

Consequently, Determine Requirements specifies the kind, quantity, location, and the intended recipients of those resources.

IKIBAN INC.

Statement of cash flow using indirect method for the year ending June 30, 2019

Particulars Amount

$

Cash flow from operating activities

Net Income 145,510

Adjustments to reconcile net income to net cash provided by operating activities

Adjustment for non cash effects

Depreciation 81,600

Gain on sale of equipment -4,300

Change in operating assets & liabilities

Increase in accounts receivable -25,500

Decrease in inventory 34,200

Decrease in prepaid expenses 3,300

Decrease in accounts payable -16,500

Decrease in wages payable -11,300

Decrease in income taxes payable -2,700

Net cash flow from operating activities (A) 204,310

Cash Flow from Investing activities

New equipment purchased -80,600

Equipment sold 12,300

Net cash flow from Investing activities (B) -68,300

Cash Flow from Financing activities

Cash dividends paid -162,310

Common stock issued 83,000

Notes payable paid -30,000

Net cash flow from Financing activities (C) -109,310

Net Change in cash = A+B+C $26,700

Beginning cash balance $67,000

Closing cash balance $93,700

Option (B) is the right choice. Explanation: Calculating the depreciable basis involves subtracting residual value from cost, which here results in $190,000 - $10,000, giving us $180,000. The usage is identified as 75,000 bolts. The first-year figures indicate the book value starts at $190,000, while 15,000 bolts were created, translating the depreciation expense into 15,000 multiplied by $2.40, equal to $36,000. Subsequently, the ending book value becomes $190,000 minus $36,000, resulting in $154,000. For Year 2, using 19,000 units leads to a depreciation expense of $45,600. The concluding book value for Year 2 becomes $108,400, while accumulated depreciation for both years culminates at $81,600.