Answer:

additional revenue = $26,250

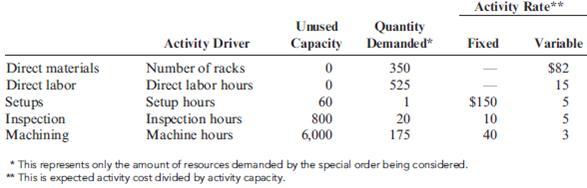

relevant costs:

direct materials = 350 x $82 = $28,700

direct labor = 525 x $15 = $7,875

setup hours = 1 x $5 = $5

inspection costs = 20 x $5 = $100

machining = 175 x $3 = $525

total relevant costs = $37,205

1) change in income if order is accepted:

total revenue - total relevant costs = $26,250 - $37,205 = -$10,955

the company will incur a loss of $10,955 if the order is approved.

2) if the cost of direct materials is decreased by $13 per unit = $13 x 350 = $4,550, and if direct labor can be reduced by 0.5 hours per unit = 175 hours (= 175 x $15 = $2,625) ⇒ total relevant costs will be lowered by $7,175.

It results in a $3,780 (= $10,955 - $7,175) loss if the special order is accepted.

Answer:

Net Present Value = $ 34,310.45

Explanation:

The Net Present Value (NPV) represents the difference between the present value of cash inflows and outflows. A positive NPV indicates a favorable investment decision, while a negative value suggests otherwise.

NPV of a project

NPV = Present Value of Cash inflows - Present Value of Cash outflow

The cash inflow is characterized as an annuity.

Present Value of annuity= A × 1 - (1+r)^(-n)/r

A refers to Annual cash flow, - 65,000, r is the discount rate at 12%, and the term is 5 years.

Calculation for Present Value of cash inflow equals 65,000 × (1 - (1.12)^(-5)/0.12) = 234,310.45.

The initial investment is 200,000.

Thus, the Net Present Value calculation is - 234,310.45 -200,000 = 34,310.45

Net Present Value = $ 34,310.45

The salvage value applied in this case is B. $20,000.

For year 3, the depreciation amounts to $80,000 calculated using the sum of the Years' Digits method on an asset with a purchase price of $500,000 and a useful life of 8 years. The salvage value taken into account for the depreciation calculations stands at $20,000.

1) Month Sales

April $299,000

May $337,000

June $387,000

Schedule of anticipated collections

For June, 202x

Cash sales in June = $387,000 x 40% = $154,800

Collections from June's credit sales = $232,200 x 20% = $46,440

May's credit sales collections = $202,200 x 50% = $101,100

April's credit sales collections = $179,400 x 26% = $46,644

Total cash collections in June = $348,984

Month DM purchases

April $44,000

May $55,000

June $55,000

Schedule of expected cash outflows for direct material purchases

For June, 202x

Cash purchases in June = $55,000 x 50% = $27,500

Cash payments for May's purchases = $27,500 x 40% = $11,000

Cash payments for April's purchases = $22,000 x 60% = $13,200

Total cash payments in June = $51,700

2) Month Sales

April $299,000

May $337,000

June $387,000

Schedule of expected collections

For June, 202x

Cash sales in June = $387,000 x 40% = $154,800

Collections from June's credit sales = $232,200 x 30% = $69,660

May's credit sales collections = $202,200 x 50% = $101,100

April's credit sales collections = $179,400 x 18% = $32,292

Total cash collections in June = $357,852

It would be beneficial to compensate the collector, as the 2% decline in uncollectible accounts outweighs the $1,000 they would earn.

3) Month DM purchases

April $44,000

May $55,000

June $55,000

Schedule of expected cash outflows for direct material purchases

For June, 202x

Cash purchases in June = $55,000 x 40% = $22,000

Cash payments for May's purchases = $33,000 x 40% = $13,200

Cash payments for April's purchases = $26,400 x 60% = $15,840

Total cash payments in June = $51,040

Cash payments will see a slight reduction in June.