Rhanda Merchandising Inc.

Income Statement

Total revenue $2,980,000

-Cost of goods sold ($1,520,828)

Gross profit $1,459,172

-Depreciation expense ($250,000)

Operating profit $1,209,172

Gain on condemnation of company property $266,000

-Loss of assets from meteor strike ($656,000)

Income from continuing operations before taxes $819,172

-Income taxes ($207,000)

Income from continuing operations after taxes $612,172

Gain from discontinued operations $755,000

-Loss from discontinued operations ($475,000)

Net income $892,172

Answer:

A) $1.82

Explanation:

The dividends discount model calculates stock value based on dividends distributed and the required return rate:

current dividend $0.20 per share

dividends for year 1 = $0.23 per share

dividends for year 2 = $0.2645 per share

dividends for year 3 = $0.3042 per share

dividends for year 4 = $0.35 per share

After year 4, we compute the growing perpetuity as follows: dividend / (return rate - growth rate) = $0.35 / (17.4% - 2.5%) = $0.35 / 14.9% = $2.35

Next, we find the present value of the cash flows:

PV = $0.23/1.174 + $0.2645/1.174² + $0.3042/1.174³ + $0.35/1.174⁴ + $2.35/1.174⁵ = $0.1959 + $0.1919 + $0.188 + $0.1842 + $1.0537 = $1.82

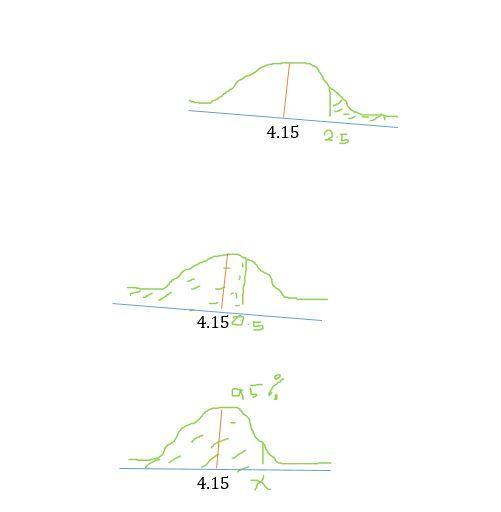

Answer:

(a)

(b)

(c) X=4.975 percent

Explanation:

(a) Identify the z-value that represents 5.40 percent

.

Thus, a net interest margin of 5.40 percent stands at 2.5 standard deviations above the average.

From the standard normal distribution table, the area to the left of 2.5 is 0.9938. Hence, the likelihood of a randomly selected U.S. bank achieving a net interest margin greater than 5.40 percent is 1-0.9938=0.0062

(b) The z-value corresponding to 4.40 percent is  The net interest margin of 4.40 percent is situated at 0.5 standard deviation above the average.

The net interest margin of 4.40 percent is situated at 0.5 standard deviation above the average.

According to the normal distribution table, the area to the left of 0.5 is 0.6915

Thus, the probability of a randomly chosen U.S. bank having a net interest margin below 4.40 percent equals 0.6915

(c) The z-value indicating 95% is 1.65

Substituting 1.65 into the equation enables us to find X.

For a bank that wishes for its net interest margin to fall below that of 95 percent of all U.S. banks, it should aim for a net interest margin of 4.975 percent.

First, it is necessary to record the depreciation expenses for January, February, and March: Depreciation expense over the three months is calculated as ($42,000 - $5,000) x 3/60 = $1,850. As of April 1, the journal entries for the depreciation expense for January, February, and March shall reflect Dr Depreciation Expense 1,850 and Cr Accumulated Depreciation 1,850. Consequently, the book value of the truck becomes $12,400 - $1,850 = $10,550. 1) In the scenario where the truck sells for $12,000 on April 1, the entries will be: Dr Cash 12,000, Dr Accumulated Depreciation 31,450, Cr Gain from Sale 1,450, and Cr Truck 42,000. If it instead sells for $9,000, the entries will adjust to: Dr Cash 9,000, Dr Accumulated Depreciation 31,450, Dr Loss from Sale 1,550, and Cr Truck 42,000. 2) Any gain or loss from the truck's sale should be recorded on the income statement under gains or losses from asset sales. 3) If Swann adopts IFRS and there was a revaluation surplus recorded on the truck, upon selling it for $12,000 on April 1, the entries should show: Dr Cash 12,000, Dr Revaluation Surplus 4,000, Dr Loss from Sale 1,450, and Cr Truck 14,550.

<span>Kathy takes on the role of Discussion Leader in the group conversation. This position is crucial as she must guide the discussion, setting expectations for the participants while allowing them adequate opportunity to share their thoughts.</span>