Answer:

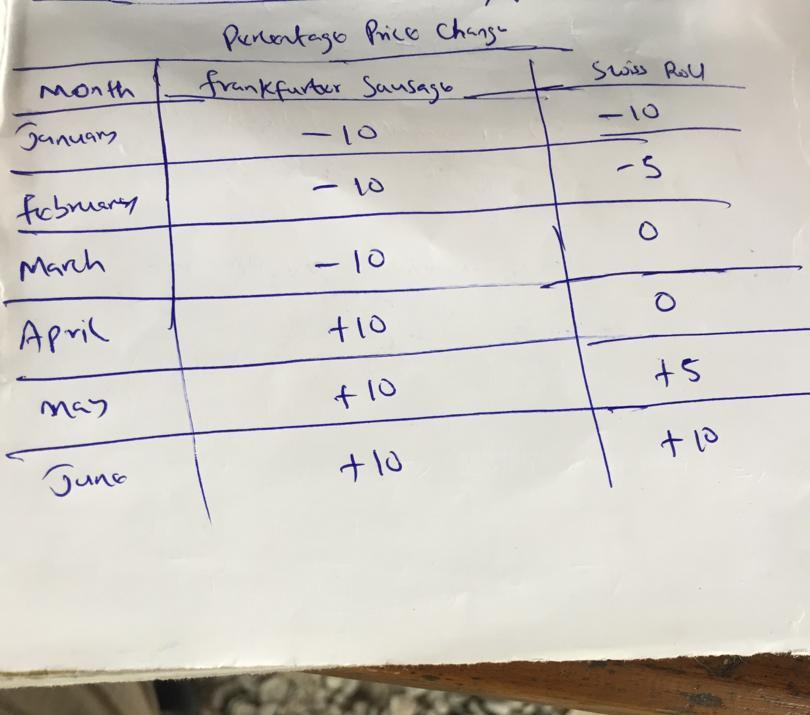

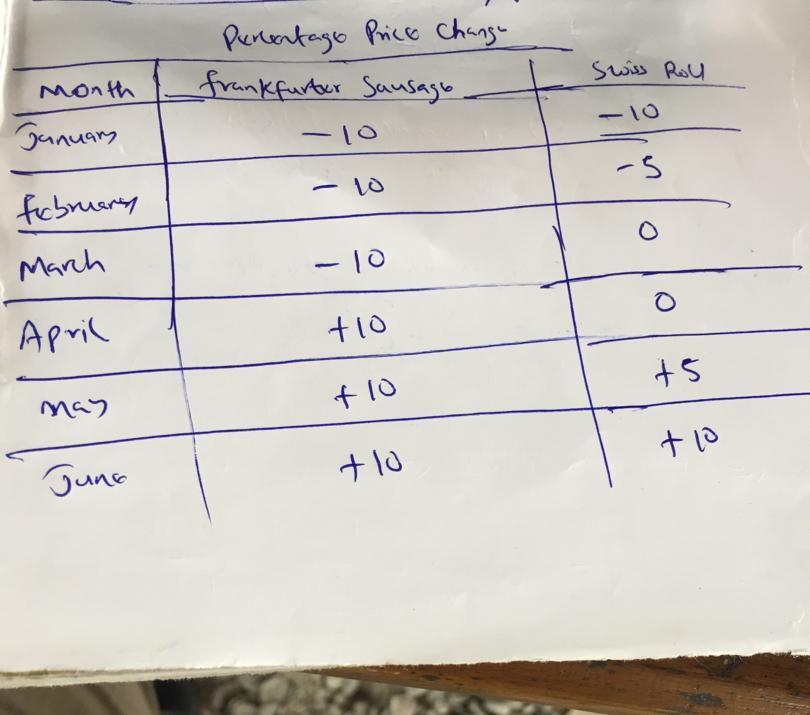

Greetings, your inquiry seems to lack detail; below is the full question along with the missing table

Your investment bank has allocated $100 million in stocks of the Swiss Roll Corporation while holding a short position in Frankfurter Sausage Company. The recent stock price history for both companies is as follows: based on the last six months, how much should your short position in Frankfurter Sausage be to adequately hedge against fluctuations in the Swiss Roll stock price?

response: $42003667

Clarification:

$100 million invested in stocks

Utilizing the data presented in the attached table below, the calculation to short Frankfurter in order to hedge the investment in Rolls is as follows

we must determine the total returns for both the Roll corporation and Frankfurter Sausage

for f-sausage

∑ (1 + monthly returns ) / 100

= ( 1 - 0.1 + 1 - 0.1.... + 1 + 0.1 ) = -0.0297 = -2.97%

for Roll corporation

∑ (1 + monthly returns ) / 100

= ( 1 - 0.1 + 1 - 0.05.... + 1 + 0.1 ) = -0.012475 = - 1.24%

next we will compute the total loss incurred from investing in Roll corporation

Total loss = percentage loss * total investment

= 0.012475 * $100 million = - $ 1247500

we will need to compensate for the loss by shorting investments in F sausage

thus: $1247500 = investment in sausage * total return

1247500 = investment in sausage * 0.0297 ( The total return of F sausage is positive because it was a short position )

therefore, to cover the loss from the ROLLS INVESTMENT by shorting F sausage

= 1247500 / 0.0297 = $42003667